| Model | Data | Accuracy | Precision | Recall | F1 | ROC-AUC |

|---|---|---|---|---|---|---|

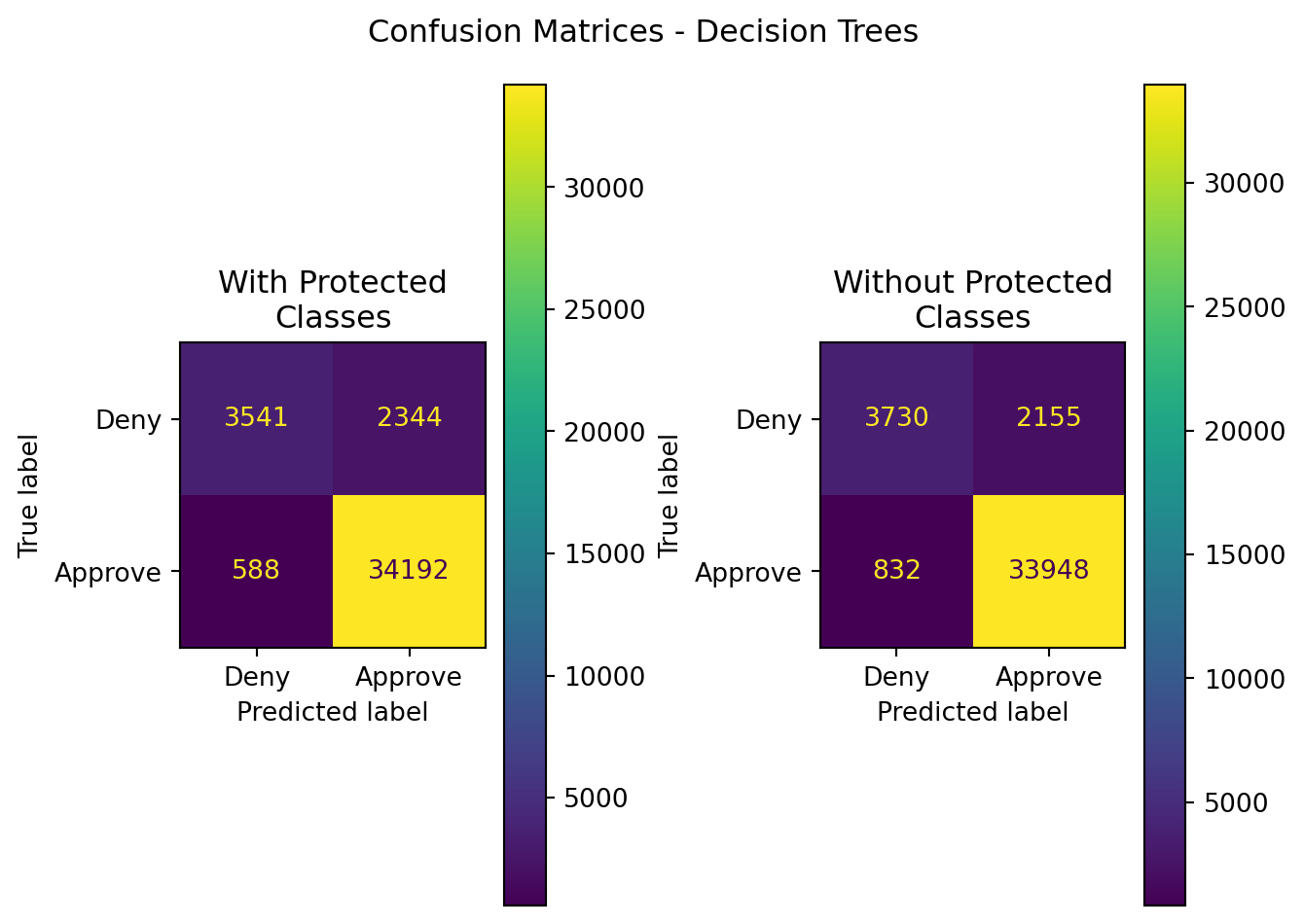

| Random Forest | With Protected Classes | 0.927899 | 0.935844 | 0.983094 | 0.958887 | 0.792396 |

| Random Forest | Without Protected Classes | 0.926546 | 0.940310 | 0.976078 | 0.957860 | 0.804946 |

11 Ensemble Modeling

11.1 Overview

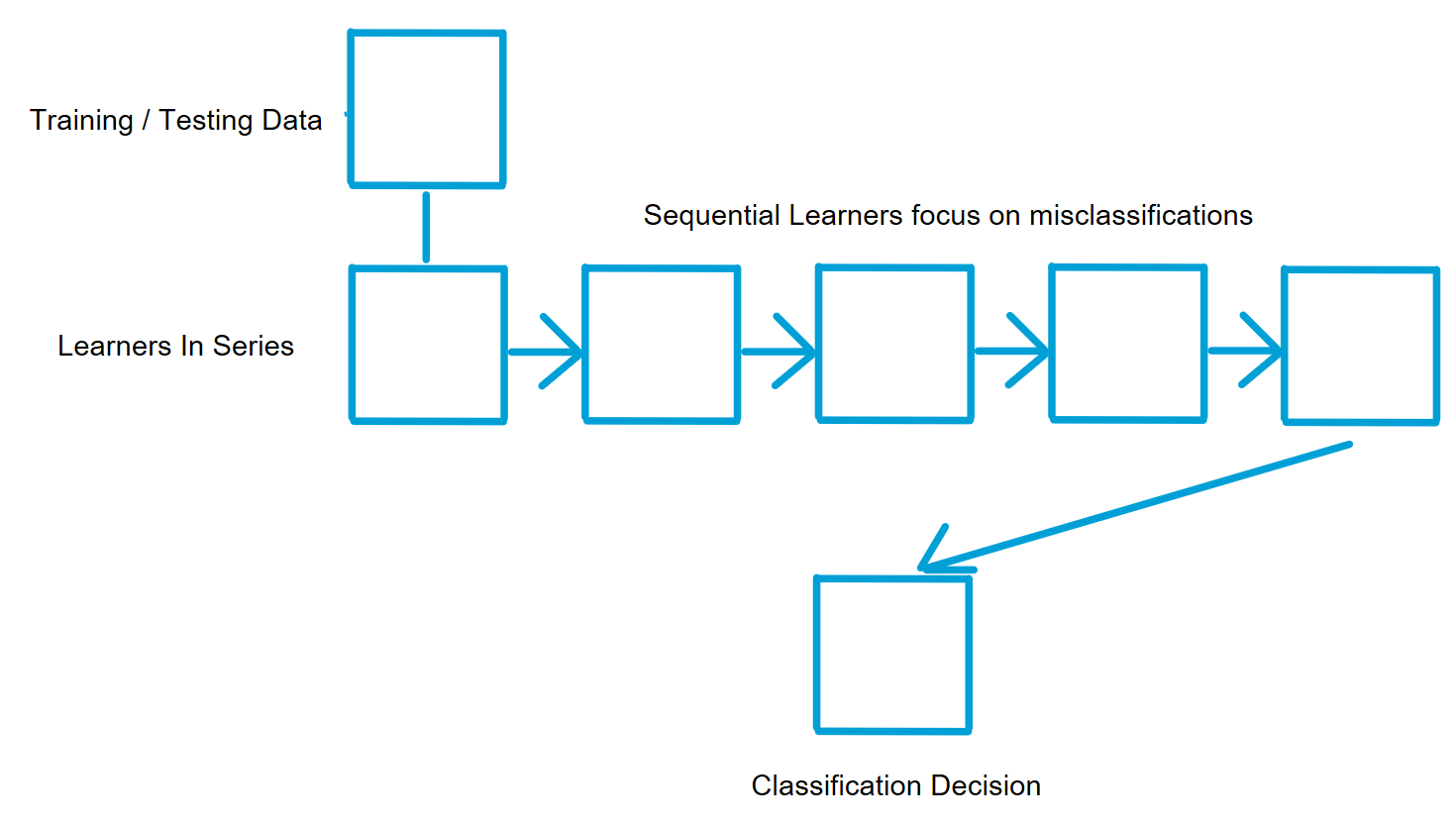

Ensemble methods are a combination of machine learning algorithms that are trained separately (either in series or parallel), and their outputs are combined to determine the classification of a given new vector of data. This provides a method that can improve predictive performance of a model, mitigate issues of model overfitting, as one model may be overfit to the data, but other independently or separately trained models can not have such overfit, and as a result, better balance the bias-variance curve of the output predictions overall for the model. What is meant by series and parallel, though?

11.1.1 Bagging

Bagging is a parallel method. This means that each model is trained independently of one another on separate random subset samplings of the source training data. Each model is then optimized for that subset of the data, and each model gets a vote in the classification of a testing datapoint. Because of this voting process, the output tends to have an odd number of models that are independently trained (at least for binary classification systems differentiating between a positive and negative outcome). Random Forests are an example of a bagging ensemble learning method.

By training multiple models simultaneously and independently, and training them on different subsets of the rows and columns of the source training data, each model develops its own unique mathematical perspective of the data. Some models may “see” features and variables that are relevant that the other models do not, and vice-versa. By developing these unique data viewpoints, the combination of models together has the potential to become stronger than any one model on its own.

11.1.2 Boosting

Boosting is a series method. For models trained in series, each subsequent model is trained based on the outcomes of the previous model, tending to focus more on records that were misclassified by the previous model. In this way, the subsequent models identify those misclassified records while still retaining appropriate predictive performance on the previous correctly classified records. In boosting, a sequence or series of weak learners are combined, with each feeding the next model in the series to improve upon the misclassified records of the previous model. The focus on misclassification allows the chain of simpler, weaker, base learning models to work together and improve overall predictive performance. This can be particularly effective with binary classifiers (that predict a yes or no outcome) as a result of the model.

An example of a boosting algorithm is called Adaptive Boosting (or ADABoost). This method examines a series of weaker classification models and assigns weights to each based upon their performance. The weight assigned to each model is based upon its output error rate - the higher the error rate, the lower the weight it is assigned.

Boosting, through focus on classification errors, does progressive clean up of prediction results, arriving at a point where, similar to bagging, the combined result of all the base learners in the chain has the potential to produce better or stronger predictive results than any one classifier on its own.

11.1.3 Random Forests

Random forests take the decision tree algorithm as described in Chapter 8, and trains multiple decision trees using that algorithm in parallel, on differing subsets of the rows and columns of the training dataset. Each tree gets a vote on the classification of new records after the training process. As such, random forests are quite popular in implementation because of their simplicity and ease of implementation.

11.1.4 XGBoost

Extreme Gradient Boosting (XGBoost) is another popular method for implementing ensembles. Its construct is similar to that of random forests, and also leverages ideas like those in logistic regression and support vector machines - identifying a gradient that can be minimized or maximized. In the case of XGBoost, the gradient optimization targets the gradient of the prediction error (akin to mean squared error in linear regression), and assigns weights to each tree within the model to minimize said prediction error. In this sense, XGBoost is a weighted voting algorithm that is akin to the performance of a neural network, but in lieu of neurons, uses the outcomes of multiple independently constructed decision trees.

11.2 Data and Code

Data for this section leverages the same data as for decision trees and can be found here:

Code to execute XGBoost and Random Forests can be found in (app-Ensemble?).

11.3 Results

| Model | Data | Accuracy | Precision | Recall | F1 | ROC-AUC |

|---|---|---|---|---|---|---|

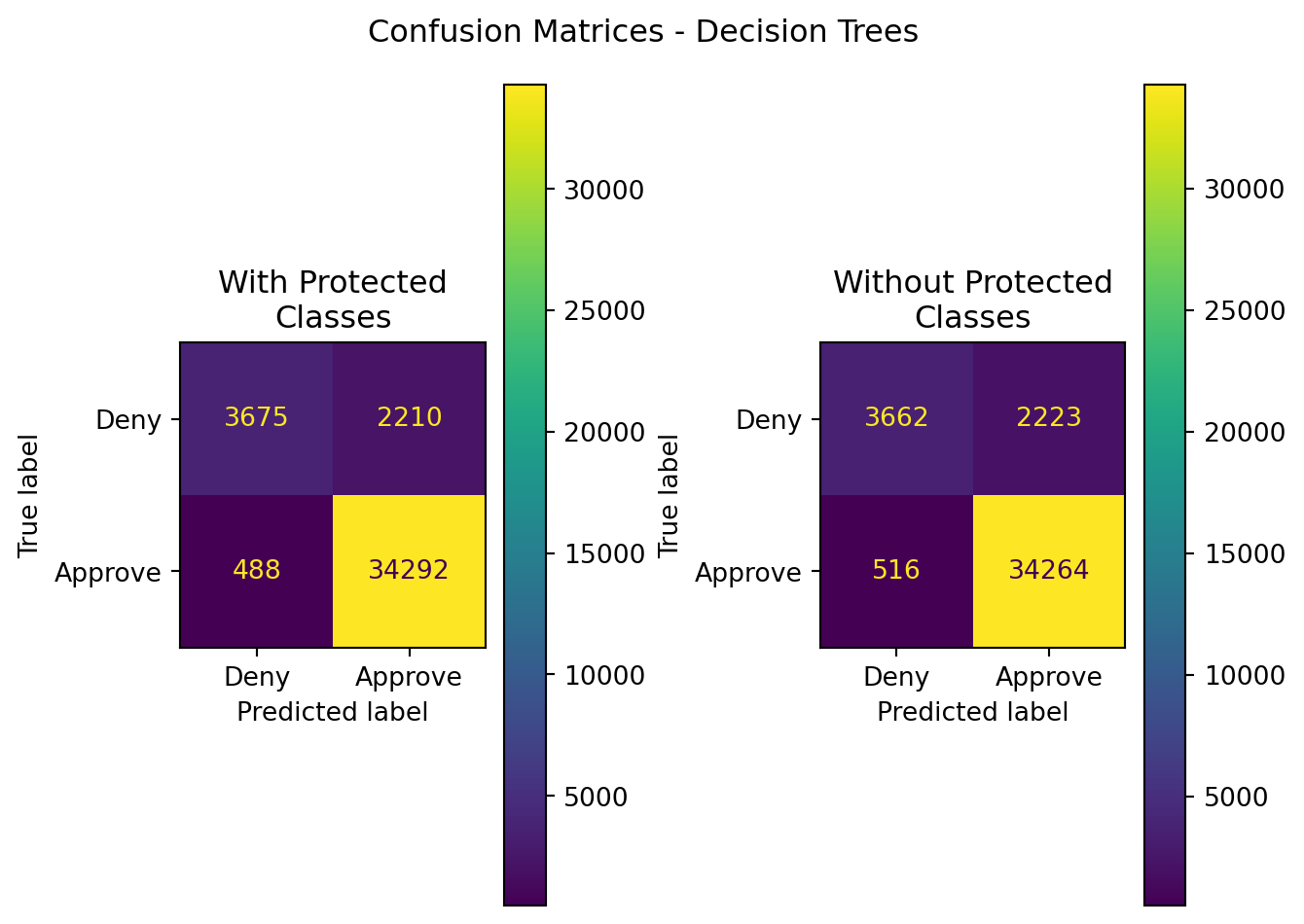

| XGBoost | With Protected Classes | 0.933653 | 0.939455 | 0.985969 | 0.962150 | 0.805219 |

| XGBoost | Without Protected Classes | 0.932645 | 0.939074 | 0.985164 | 0.961567 | 0.803712 |

Of these two ensemble methods, one can see that XGBoost outperformed Random Forest classification. However, the results compared to those in the other sections examining Bernoulli Naive Bayes, Logistic Regression, and Support Vector Machines far outshine the performance of XGBoost - especially when comparing ROC-AUC.

Both of these models had a more rapid time for training, fitting, and predicting outcomes, at the cost of accuracy and other model performance metrics.

In the case of XGBoost, a single test appears to favor the inclusion of protected class data. While that is the case, the difference in performance is less than 1% across all metrics. Is this statistically significant?

| Stat | z-score | p-value | top performer | top mean | difference in means |

|---|---|---|---|---|---|

| Accuracy | 0.177171 | 0.859374 | With Protected Classes | 0.934603 | 0.000011 |

| Precision | 4.179453 | 0.000029 | With Protected Classes | 0.940035 | 0.000229 |

| Recall | -6.218760 | 0.000000 | Without Protected Classes | 0.986727 | 0.000260 |

| F1 | -0.107982 | 0.914010 | Without Protected Classes | 0.962694 | 0.000004 |

| ROC-AUC | 3.743439 | 0.000182 | With Protected Classes | 0.807282 | 0.000676 |

In short - yes, statistically significant difference in performance exist, and they favor inclusion of protected classes for precision and ROC-AUC, and favor exclusion of protected classes in recall. All other p-values are above the significance threshold of \(\alpha\) = 0.003. Operationally, however - there is no real impact. The significant differences are less than a fraction of a percent and in no way shape or form justify their inclusion as a substantially better improvement over their exclusion.

Using ensemble learning methods can help mitigate risks in models such as overfitting, underfitting, and mitigating the bias-variance balance within a machine learning algorithm. While these methods can support such goals, they remain underperformers in comparison to the other modeling and work performed in this study. The 500-fold cross-validation of several other models are substantially better in performance compared to XGBoost